Case Background

Michelle L. Moriarty sued American General Life Insurance Company in the United States District Court for the Southern District of California over the company's refusal to pay a $1,000,000 life insurance benefit after her husband died. She brought the case individually, as successor-in-interest to her late husband Heron D. Moriarty, on behalf of his estate, and on behalf of a proposed class of policyholders and beneficiaries.

Cause

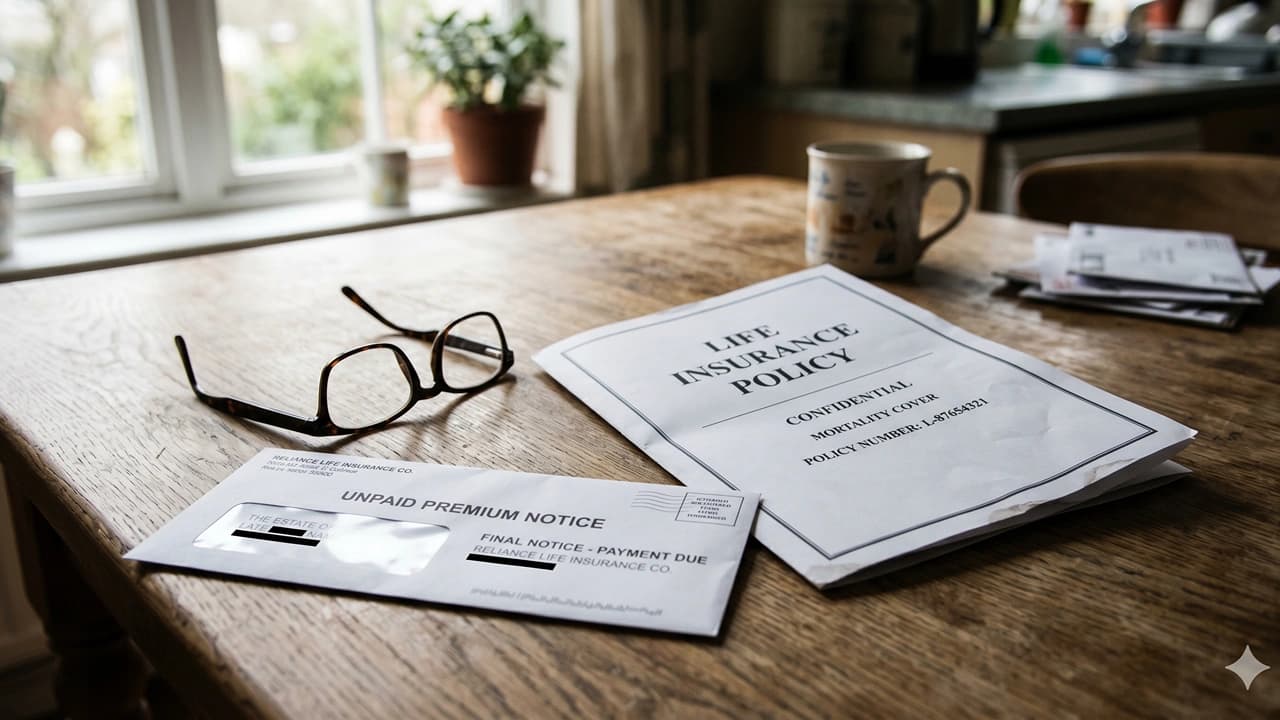

In September 2012, Heron Moriarty bought a $1,000,000 term life insurance policy and named his wife as the sole beneficiary. He paid the monthly premiums, due on the 20th of each month, from September 2012 onward. On March 20, 2016, a prearranged debit payment to the insurer was rejected. American General said it sent a letter on March 24, 2016, telling Moriarty the premium had not been paid, and then claimed it sent a termination notice on May 22, 2016, stating the policy had ended on March 20, 2016, for nonpayment. Moriarty, who was incapacitated at the time, died on May 31, 2016.

Moriarty argued that the insurer never followed two California Insurance Code provisions, Sections 10113.71 and 10113.72, which took effect on January 1, 2013. Those laws gave policyholders a 60-day grace period before a policy could lapse, a right to a written 30-day notice before any termination, and an annual right to name another person to also receive lapse and termination notices. She said her husband never received notice of his right to designate another person, never got a 60-day grace period, and never received a 30-day written notice before the policy ended. American General took the position that these provisions did not apply to policies issued before January 1, 2013, calling that an illegal retroactive application of the law. Moriarty countered that the statutes applied to every policy in force on January 1, 2013, and only governed how policies could be lapsed or terminated after that date.

Injury

After her husband died, Moriarty filed a claim for benefits on June 24, 2016. American General denied the claim on July 26, 2016, citing only the policy's lapse for nonpayment on March 20, 2016. Moriarty supplemented her claim several times, pointing to the California Insurance Code provisions and Court decisions interpreting them, but the insurer continued to refuse payment. As a result, Moriarty lost the policy benefit meant to protect her family, and she said she suffered emotional distress along with the cost of hiring lawyers to pursue the claim.

Damages Sought

Moriarty asked the Court to certify the case as a class action and to declare the rights of the Plaintiff and the proposed classes under the policies. She sought an injunction against American General, economic damages for the classes according to proof, and economic, noneconomic, punitive, and exemplary damages for herself individually against the insurer. She also requested attorneys' fees, litigation costs, and any other relief the Court found proper.

Key Arguments and Proceedings

Legal Representation

Plaintiff: Michelle L. Moriarty, individually, as successor-in-interest to Heron D. Moriarty, on behalf of his estate, and on behalf of the class.

· Counsel for Plaintiff: Craig M. Nicholas | Alex M. Tomasevic | Shaun Markley | Jack B. Winters, Jr | Georg M. Capielo | Sarah Ball | Michelle Marie Meyers

Defendant: American General Life Insurance Company, a Texas corporation. Bayside Insurance Associates, Inc., a California corporation, was also named as a Defendant in the complaint.

· Counsel for Defendant: Nicholas J. Boos | Tara L. Blake | Caleb C. Wolanek | Michael D. Mulvaney | Thomas J. Butler | Christopher Charles Frost | David J Noonan

Key Arguments or Remarks by Counsel

The dispute centered on whether the California Insurance Code provisions reached a policy issued before January 1, 2013. Moriarty's lawyers argued the statutes used the word "every" and contained no language limiting them to newly issued policies. They pointed out that when the Legislature wanted to limit a rule to new policies, it said so plainly, as it did in another section of the code. American General maintained that applying the provisions to an older policy amounted to an improper retroactive use of forfeiture rules.

Claims

Moriarty raised several claims against American General. She sought declaratory relief asking the Court to confirm that the two statutes applied to policies issued before January 1, 2013, and in force on that date. She claimed breach of contract, saying the insurer ignored the grace period, the 30-day notice rule, and the annual designation notice, then refused to pay benefits. She claimed bad faith, arguing American General knew California Courts had ruled the statutes applied to older policies yet still denied the claim, which she said justified punitive damages. She also brought a claim under California Business & Professions Code Sections 17200 for unlawful business practices.

Against Bayside, Moriarty brought a negligence claim. She said she contacted Bayside agents on April 25, 2016, to ask what steps to take to prevent the loss of the insurance, and that on April 26, 2016, Bayside told her it would contact American General and advise her what to do. She alleged Bayside never investigated or followed up.

Defense

Bayside filed an answer denying the core allegations. It admitted that Moriarty purchased a term life policy and that Bayside brokered the sale, and it admitted Moriarty contacted the company on April 25, 2016, believing a premium had not been paid. But Bayside denied that she asked what steps to take to prevent loss of the insurance, denied that it had received any lapse notice as of that date, and denied that it failed to assist her. Bayside also raised thirteen affirmative defenses, including failure to state a cause of action, estoppel, waiver, laches, and unclean hands. American General's position throughout was that the policy had lapsed for nonpayment and that the statutes did not apply.

Jury Verdict

The case went to trial before Judge Jinsook Ohta, with the trial date listed as January 12, 2026. Before the jury deliberated, the Court had already decided two points: that California Insurance Code Sections 10113.71 and 10113.72 applied to Mr. Moriarty's policy, and that American General violated California law by failing to tell him of his right to name another person to receive notices of unpaid premiums and pending termination, so no 30-day termination notice went to a designated person.

On January 13, 2026, the jury returned its verdict in favor of the Plaintiff. The jury found that Mr. Moriarty did not knowingly or intentionally allow his policy to lapse. It found that American General's failure to notify him of his right to designate another person caused the policy to lapse. It also found that the company's failure to send a 30-day notice of pending lapse to a designated person caused the lapse of the policy.

Court documents are available upon request at [email protected]